Describe Some Methods Used to Allocate Support Costs

Cost Allocation Based on Sales. Costs are allocated based on the profits generated by each.

Cost Allocation Illustrated Mgt231 Lecture In Hindi Urdu 26 Youtube Cost Allocation Lecture Hindi

In determining which support department cost allocation method to use companies must.

. The direct method - Each support departments costs are allocated among the production departments that consume part of the support departments output. It allows reflection of all reciprocal services among service departments. The direct sequential and reciprocal methods.

1 the direct method. Since high sales volume does not necessarily equate to high profits this approach can result in a low-profit entity being burdened with a substantial corporate allocation. The direct allocation method reciprocal allocation method step.

There are three methods for allocating service department costs. Interview Questions And Answers Guide Global Guideline - Interviewer and Interviewee Guide. However once a service departments costs have been allocated no subsequent costs are allocated back to it.

The direct method allocates support department costs only to the operating departments. In determining which support department cost allocation method to use companies must. The direct method the step-down method and the reciprocal method.

An advantage of this approach is simplicity. There are three methods commonly used to allocate support costs. 4 The process continues until all service department costs are allocated.

2 the sequential or step method. Three methods which are used to allocate costs of support departments are. Costs are apportioned based on the net sales reported by each entity.

Three methods can be used to allocate support department costs. There are three methods commonly used to allocate support costs. Three methods can do the cost allocation from the service department in the manufacturing department.

Three methods can be used to allocate support department costs. Weigh the costs and benefits associated with each method. Distinguish between two methods of allocating costs.

Cost Allocation Based on Profits. Determine the extent of support department interaction. Allocates support-department costs to other support departments and to operating departments in a sequential manner that partially recognizes the mutual services provided among all support departments.

Can you describe some of the methods used to allocate support costs. Theoretically this method is the most appropriate for allocating service department costs. Simultaneous equations are used to compute the completed reciprocated cost.

There are three methods of support department cost allocation. Job Interview Question Describe Some Of The Methods Used To Allocate Support Costs. The direct method allocates costs of each of the service departments to each operating department based on each departments share of the allocation base.

And 3 the reciprocal method. - This method ignores the fact that some support departments provide services to other support departments 2. Three methods which are used to allocate costs of support departments are.

Job Interview Question Explain Some Of The Methods Used To Allocate Support Costs. The direct sequential and reciprocal methods. The direct method the step-down method and the reciprocal method.

Stand-alone- uses information pertaining to each user of a cost object as a separate entity to determine cost allocation weights Incremental- ranks individual users of a cost object in the order of most responsible for common costs and then ranking is used to allocate costs among those users. Determine the extent of support department interaction. The choice of which department to start with is very important.

1 the direct method. A disadvantage of the approach is that it does not take into account the extent to which some. Services used by other service departments are ignored.

An advantage of this approach is simplicity. And 3 the reciprocal method. The first method the direct method is the simplest of the three.

The step-down method or known as sequential method allocates the costs of some service departments to other service departments. Direct method Step method Reciprocal method Direct Method A firm generates various expenses that can be assigned to a specific cost item such as a commodity program function or service. In the examples below we used the square footage and the.

3-The reciprocal method a. Assigning Budget versus Actual Service Costs. When allocating costs there are four allocation methods to choose from.

2 the sequential or step method. The direct method allocates support department costs only to the operating departments.

Peanut Butter Costing Meaning Example Drawbacks And More Learn Accounting Bookkeeping Business Accounting And Finance

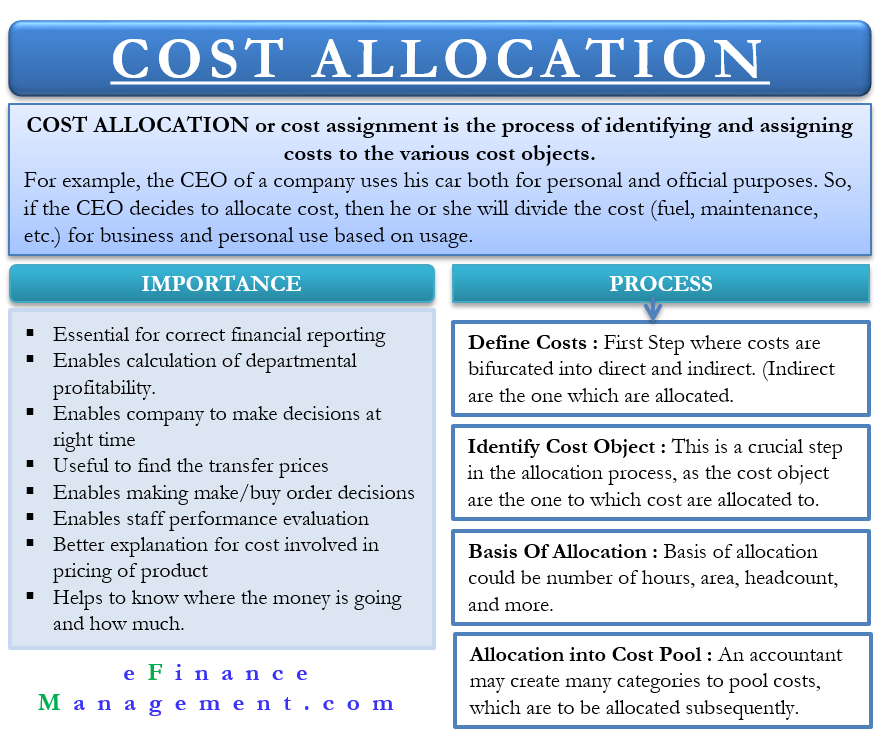

Cost Allocation Meaning Importance Process And More

Master Budgeting And Responsibility Accounting Mgt231 Lecture In Hindi Urdu 10 Youtube Budgeting Accounting Lecture

C2 1 Learning Objectives 1 Usefulness Of An Account 2 Characteristics Of An Account 3 Analyzing And Summarizi Learning Objectives Financial Analysis Learning

0 Response to "Describe Some Methods Used to Allocate Support Costs"

Post a Comment